Činilo se kao da će Europa (euro-zona) izbjeći ekonomski “napad” iz Amerike i proći najgori dio globalnog usporavanja. Možda, ali znakovi za sada ukazuju da to neće biti baš tako. Sa ekonomijom od oko $12.2 bilijuna, euro-zona je druga po veličini nakon Američke. Da li će upasti u recesiju ili “samo” tvrdo pasti još se  ne zna. Po nekim analitičarima, upravo je izgledno da će EU pasti u recesiju, dok će se Američka polako i otegnuto izvući ili je za dlaku izbjeći. Po drugima, Američka je već u recesiji koji mjesec. Recimo da je priča jednostavna: Od 2001. najveće ekonomije Njemačka i Francuska su bile potištene. Male zemlje, Irska i Španjolska su izvlačile Europu izvozom u Britaniju i van europe, te nekretninskim boom-om. Sada se nekretninski boom preokrenuo, jaki euro smanjuje izvoznu konkurentnost, Britanija i Amerika su rastom gdje su Njemačka i Francuska bile većinu ovog desetljeća + kreditna kriza + nafta od $140 + neugodna inflacija.

ne zna. Po nekim analitičarima, upravo je izgledno da će EU pasti u recesiju, dok će se Američka polako i otegnuto izvući ili je za dlaku izbjeći. Po drugima, Američka je već u recesiji koji mjesec. Recimo da je priča jednostavna: Od 2001. najveće ekonomije Njemačka i Francuska su bile potištene. Male zemlje, Irska i Španjolska su izvlačile Europu izvozom u Britaniju i van europe, te nekretninskim boom-om. Sada se nekretninski boom preokrenuo, jaki euro smanjuje izvoznu konkurentnost, Britanija i Amerika su rastom gdje su Njemačka i Francuska bile većinu ovog desetljeća + kreditna kriza + nafta od $140 + neugodna inflacija.

- Britanski mjehur na tržištu nekretnina je prsnuo. Prodaja kuća je na najnižem levelu u posljednjih 30 godina. Stopa inflacije od 3.8% najviša u posljednjih 10 godina. (Visoka inflacija dok cijene kuća padaju?) Kao i drugdje u Europi povjerenje potrošača je nisko. Britanija je najveća europska ekonomija van 15-članske euro-zone.

- Mjehur nekretnina je prsnuo i u Irskoj i zemlja se nalazi na rubu recesije. Cijene kuća su pale otprilike 15% ove godine uz predviđanje da će padati sve do pošetka sljedeće. Iako su neki drugi djelovi ekonomije dobri, izvoz primjerice, pad cijena na tržištu nekretnina je toliko velik da je izbrisao rast drugdje. Zapravo, Irski Economic and Social Research Institute predviđa kontrakciju gospodarstva ove godine od 0.4 posto, naspram rasta od 4.5% 2007. U prvom kvartalu BDP je pao 1.5%.

- U Španjolskoj je građevinska tvrtka Martinsa-Fadesa, sa imovinom od €10.8 milijardi objavila bankrot i tako postala najvećom žrtvom prskajućih europskih nekretninskih balona (porast cijena nekretnina u Americi u usporedbi sa euro-zonom je bio blag) i najvećom poslovnom propašću Španjolske. Groupa MF posjeduje najveću izgrađenu površinu u Španjolskoj, 28 mil. četvornih metara i posjeduje 170,000 jedinica u izgradnji. Ni prva ni zdanja koja je propala sigurno. Građevinski boom je nestao.

- Njemački izvoz pati zbog jakog eura i slabe amerike, a potrošači su najneraspoloženiji od 1991. I Francuski potrošači, dugo stup potražnje euro-zone, su neraspoloženi. Najslabije raspoloženi od 1987.

Više o Španjolskoj Martinsa-Fadesa grupaciji, Njemačkoj, Francuskoj u WSJ članku niže. I NYT ima slični tmurni outlook.

Spain, Ireland and Denmark are either in a recession or on the brink. Italy is stagnating. France is weakening fast. And Germany, the sturdy locomotive of European growth, is suddenly faltering — dashing most residual hopes that Europe could escape the upheaval in the United States.

Bankruptcy Rocks Spain

July 16, 2008; Page A1

Just a few weeks ago, Europe thought it could escape the worst of the global slowdown. Now it looks like the euro zone, the world’s second-largest economy, is headed for a hard landing and perhaps recession, compounding growth troubles around the world.

On Tuesday, Spain suffered its largest-ever business failure as construction group Martinsa-Fadesa SA, a company with assets of €10.8 billion, or about $17.17 billion, filed for bankruptcy protection, making it the biggest victim so far of Europe’s bursting real-estate bubbles. That same day, the euro, boosted by the central bank’s inflation-fighting efforts and fears of financial-sector fragility in the U.S., briefly reached a record high of over $1.60, posing a further threat to Europe’s export sector. And an index of investor sentiment in Germany, Europe’s biggest economy, fell to its lowest level since the recession of the early 1990s.

The rising risk of recession in Europe shows that despite the strength of emerging markets such as Russia and China, the economic downturn that began in the U.S. last year is spreading to other regions. That is battering hopes that the global economy might have “decoupled” just enough from America’s that the rest of the world could ride out a U.S. slump relatively unscathed.

One sign that many investors no longer believe in decoupling: Stock markets in Europe and Asia tumbled Tuesday in the wake of the U.S. government’s rescue package for mortgage behemoths Freddie Mac and Fannie Mae. Analysts say investors fear the rescue indicates that troubles in the U.S. are severe and will hit economies elsewhere. In Tokyo, shares in Sumitomo Mitsui Financial Group, Japan’s largest bank by market value, fell 6.1%, helping to send the Nikkei 225 Stock Average Index down 2% to a three-month low. London’s FTSE 100 index fell 2.4% to 5171.9.

Europe’s banking and property sectors are increasingly feeling the fallout from the housing-market and financial-sector turmoil across the Atlantic. Although Europe had little subprime lending of its own, many European banks lost money on U.S. mortgage-related securities, causing bank funding costs to rise and forcing banks to rein in their property lending at home.

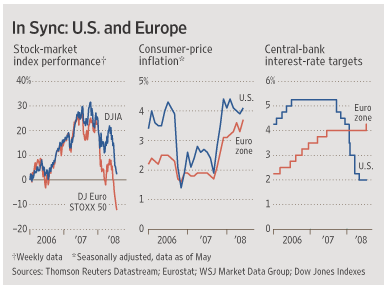

Earlier this year, the euro zone’s $12.2 trillion economy, second in size only to America’s, was looking fairly solid. Exports to emerging markets and business investment were healthy, especially in Germany, the zone’s largest single member economy. French household spending, a longtime source of growth, hadn’t sputtered. Spain’s red-hot housing market was cooling off gradually. The European Central Bank remained relatively optimistic about the bloc’s prospects. And Europe’s main stock markets began recovering, driven by hopes the Continent would weather the global storm.

But since mid-May, the European stock markets have slid. “All of the sources of growth are in trouble. It’s not clear where the recovery is going to come from,” says Michael Hume, European economist at Lehman Brothers who believes there’s a 40% chance of an outright recession in the euro currency area this year.

The critical change has come in Germany. Stung by the strong euro and rising costs, Germany’s previously booming manufacturers have suffered declining new orders for six months in a row. Blue-chip companies including engineering giant Siemens AG, consumer-goods maker Henkel AG and printing-machine maker Heidelberger Druck AG have all announced large-scale job cuts lately, blaming problems including the high euro, raw-material prices, slower global growth and the credit-market mess that has shaken confidence on both sides of the Atlantic. A stronger euro makes goods priced in the currency more expensive for buyers in the U.S. and other nations.

“I’m asking myself: Which markets are still functioning?” says Rainer Hundsdörfer, director of Michael Weinig AG, a midsize German company that makes wood-processing machines used to build furniture and fittings. He says new orders from the rest of Europe “are crumbling,” weak business in the U.S. has been made worse by the high euro, and many customers in Asia and Latin America have stopped investing in new machines because they rely on exports to the slowing U.S. economy. A backlog of orders is keeping the company busy for now, but 2009 could be a difficult year, Mr. Hundsdörfer says.

French consumer spending, once a pillar of the euro zone’s domestic demand, is also faltering on rising inflation and a weakening housing market. In June, French consumer confidence hit its lowest point since the national statistics office INSEE began tracking the measure in January 1987.

Gradual Slowdown

The ECB continues to predict the 15-nation euro zone will suffer only a gradual slowdown. At a news conference earlier this month, President Jean-Claude Trichet admitted second-quarter euro-zone growth would disappoint and warned “the third quarter will probably not be particularly flattering either,” but stressed the bloc’s “sound” fundamentals. The bank’s official forecast is that the euro-zone economy will “trough” in the second quarter and expand by around 1.8% this year and 1.5% next year.

“They are wrong,” says Olivier Gasnier, economist with Société Générale in Paris, who predicts the euro zone will grow by only 1.1% this year — thanks mainly to a first quarter whose strength probably won’t be repeated — and an anemic 0.4% next year.

And some economists believe the ECB’s emphasis on fighting inflation could worsen the downturn. While the U.S. Federal Reserve has cut its key rate by 2.75 percentage points since September, the ECB has focused on the inflationary threat of rising commodity prices, and raised its key rate by a quarter percentage point to 4.25% earlier this month.

In the period after 2001, the last time Germany and the euro zone’s core economies suffered a downturn, Spain, Ireland and other booming smaller economies helped pick up the slack. The U.K. — the biggest European economy outside the euro zone — sucked up imports. As a result, the euro zone avoided recession and began a recovery that lasted until now.

But this time, the U.K. is in bad shape, with its housing market falling sharply and inflation rising fast. Data out Tuesday showed U.K. inflation at 3.8% in June, up from 3.3% and well above expectations. The Spanish housing sector is in a deep slump, and the country’s construction-dependent economy is expected to enter a recession this year, ending a decade of strong growth. Spanish house prices fell by 0.1% in the second quarter of this year, logging their first quarterly decline in nearly a decade.

Martinsa-Fadesa’s debts outstanding of €5.2 billion make its filing for creditor protection the largest ever in Spain. The building giant’s demise is expected to send shock waves through a real-estate sector buffeted by plummeting home sales and tighter bank lending ushered in by the U.S. crisis. In 2006, Spain built more than 700,000 houses — more than Germany, France and the U.K. combined — and investment in housing made up nearly 10% of gross domestic product. But the boom peaked last year, and Spanish home-sales transactions fell by 32% in the first quarter, compared with a year earlier. In May, Spain’s unemployment rate stood at 9.9% — the highest in the euro zone — up from 8.6% at the end of 2007.

Lining Up at the Doors

At the Águeda Díez jobless-claims center in Madrid’s Carabanchel district, the unemployed are lining up at the doors from 5 a.m. every morning, according to an official who declined to be identified. “We can only attend to 300 a day. Hundreds are being turned away,” the official said. The district is home to many immigrants who found, then lost, jobs in Spain’s construction sector.

The accelerating problems in Spain’s property market signal a new and potentially more-worrisome chapter for European banks: On top of losses tied to U.S. securities markets, slowing economies and housing markets back home could now force banks to set aside yet more money to cushion against losses. That could crimp lending and lead to a spiraling downturn in Europe, economists say.

Several large Spanish banks stand to take big hits from the collapse of Martinsa-Fadesa. Banco Popular Español SA says it has provisioned €100 million against possible loan losses. Savings bank Caja Madrid says it had lent the company €1 billion, and La Caixa says it had loaned €700 million. Fear of lending losses in Spain could further drive up borrowing costs in Europe’s troubled interbank-lending market.

Moves by Swiss regulators to increase capital requirements, meanwhile, could force that country’s two biggest banks — UBS AG and Credit Suisse Group — to shrink their balance sheets significantly, analysts at Morgan Stanley said this week. More banks also are expected to cut their dividends.

–Carrick Mollenkamp in London, Christopher Bjork in Madrid and Yuka Hayashi in Tokyo contributed to this article.

Write to Marcus Walker at marcus.walker@wsj.com1, Joellen Perry at joellen.perry@wsj.com2 and Jonathan House at jonathan.house@dowjones.com3